A Degrowth Bank

The trick is - it isn't a bank.

I was in Barcelona, Spain last week for a meeting of the Post-Growth Finance Circle hosted by Research and Degrowth International (more on that later in the week). When I first arrived, I got to learn about Coop57. I regret that I was a bit jet lagged and lacked sleep, so I’m sure I missed an important point or two from the presentation by Eloi Domingo Castells, but I was quite impressed about what Coop57 is up to and thought it worth sharing

If you are a bit disappointed in the state of the financial leadership in the world, check out what COOP57 is doing, and it may just restore some of your faith in financial humanity.

Coop57 is a democratic cooperative of financial services that operates across Spain, and whose mission is to promote social and solidarity economy initiatives through financial intermediation. In 2022, they had over 37M lent to projects of its members.

But Coop57 is not a bank. The cooperative was established in 1995 in Barcelona and since its inception in Catalonia, sections have been set up in Aragon, Madrid, Andalusia, Galicia, the Basque Country and Asturias.

Coop57 defines itself as a tool of solidarity and support to help members and transform society. The essential function of Coop57 is financial intermediation. Or, it can be said, to capture savings to channel them to finance social and solidarity economy projects.

It bears repeating that Coop57 is not a bank, but a service cooperative and, therefore, all the people or entities that are related to Coop57 do so from the position of member of the cooperative, forming part of its ownership structure and participating democratically and in an assembly way in the decisions and direction of the cooperative.

Coop57 doesn’t have customers, but members.

Coop57 is a cooperative and as such operates exclusively with its members. Everyone who interacts with the cooperative does so from the position of member, they don’t refer to their members as customers. In order to save at Coop57, you must be a collaborating member of Coop57.

Being a member of Coop57 means belonging to a network of people and entities that work collectively to promote other economic and social models. It means exercising economic sovereignty and implementing financial models that take into account people, the environment and the territory instead of maximizing profits.

To be a member is to be part of a community that seeks to ensure that the funds of Coop57 are used to improve the community.

Many banks can’t have that kind of mandate, because if they are publicly traded, they have a mandate to serve shareholders (remember profit maximization is the decision rule) and not communities first.

There are two types of partners at Coop57:

Service partners: Legal entities belonging to the social economy (cooperatives, associations, foundations, insertion companies, etc.). They can receive loans from Coop57 if they become a member.

Collaborating members: Individuals or legal entities who can save to Coop57 by making contributions to the cooperative's share capital.

What is the money deposited used for?

The savings deposited in Coop57 are used to grant loans to Coop57's service partners. These entities are projects based on the principles of the social and solidarity economy and that, in order to become service partners of Coop57, have passed a rigorous ethical and social evaluation that analyzes that they are projects that provide some type of added value to society as a whole.

Once the entity is a service member of the cooperative, it can access financing. In the event that the entity so requests, a technical and financial evaluation of the viability of the project will then be carried out in order to grant that financing.

The funded projects are aimed at generating stable and quality jobs in cooperative models, social and labour insertion initiatives, social movement projects, care for vulnerable people and groups, sustainability and the environment, agroecology, fair marketing, community development, culture and education, models that promote democratic and participatory deepening or grassroots associationism, and others.

Contrast that with the decision rule at publicly traded banks, where what gets funded is what can maximize profits. The good of any community rarely enters the picture.

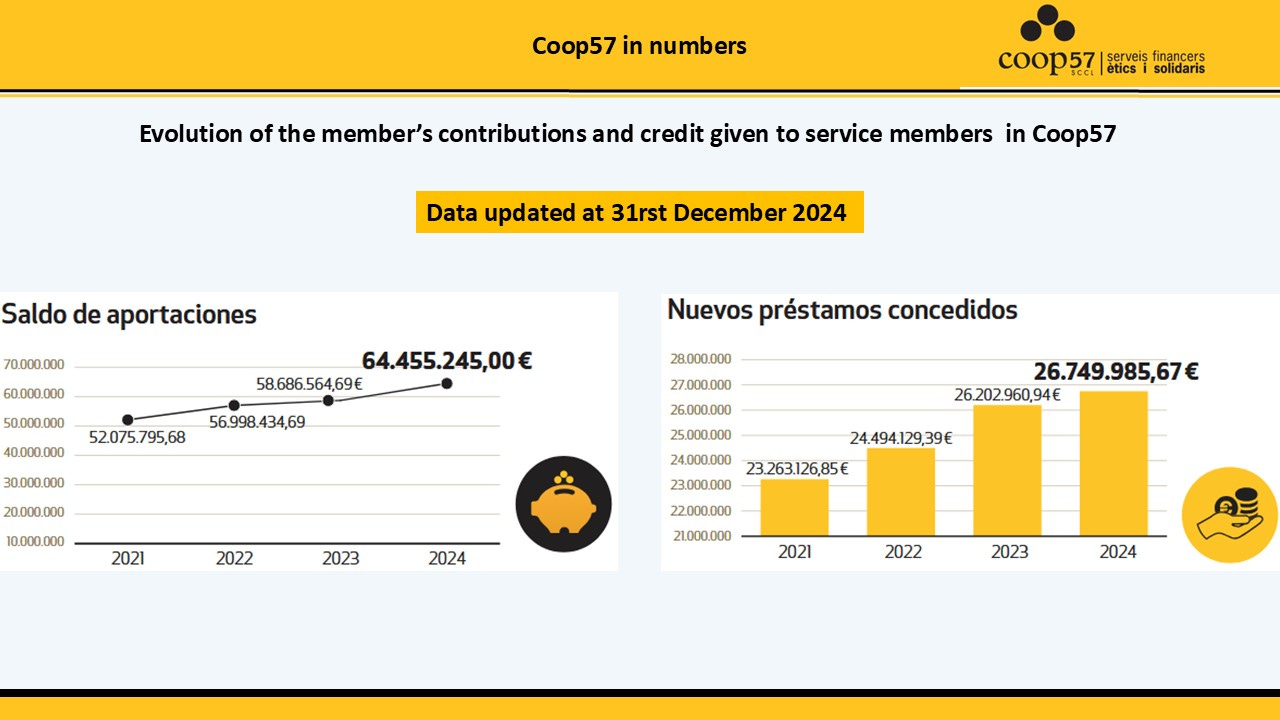

Here is a slide from the presentation I mentioned. I’ll translate. Saldo de aportaciones means “balance of contributions”. Nuevos prestamos consedidos means “new loans granted”.

You can see that although “growth” is not the goal, Coop57 has a nice growth thing going, which will allow it to serve more of the community.

How safe are the savings?

Coop57 carries out a financial activity among its members as a service cooperative. Because it is not a bank it does not have the coverage of the Bank of Spain's deposit guarantee fund. The money contributed by the members, including the collaborators, is in the form of share capital and, therefore, is responsible for the performance of the cooperative.

Coop57 is not subject to banking regulation. Instead, it is self-regulating, collectively and democratically, according to the criteria that are considered most appropriate. In this sense, the contributions, which are not guaranteed, are subject to a battery of measures to be able to guarantee these contributions from the collaborating members.

Although in many countries there are no “reserve requirements” by law, many large banks hold minimum reserves of about 5 percent of all assets in liquid assets in order to cover any calls for deposits from customers. Coop57 holds reserves of about 15 percent of the total voluntary contributions so that they have the liquidity to handle withdrawals, even in a crisis.

To strengthen its solvency, Coop57 adopts several internal measures:

It allocates its surpluses to reserves. Profits are not distributed but all are used to strengthen the solvency of the project

It requires entities that receive financing to make additional contributions to the share capital to nourish a solidarity fund to guarantee loans

Allocate the maximum possible for provisions (that money reserved to deal with possible eventualities) for possible defaults

It limits the maximum loan limit that a member entity can receive and, thus, distributes the risk (at most, an entity cannot receive more than 2% of the resources available to Coop57 in loans)

Because it is not a bank, COOP57 doesn’t offer some traditional bank services.

Coop57 cannot offer commercial banking services and therefore, cannot offer current accounts, direct debits, transfers to third parties, credit/debit cards, or similar banking operations.

People who have money at Coop57 do so in the form of a contribution to the cooperative's share capital and, although new contributions can be made and/or refunds can be requested whenever you want, it must be interpreted more as a savings space than as an account in which to carry out daily operations.

The Principles they are governed by.

At Coop57 says that it accepts and promote the principles of ethical finance. There are 5 fundamental principles:

Principle of applied ethics: application of non-economic criteria in savings and investment decisions.

Principle of participation: decisions are made democratically with the participation of the partners.

Principle of coherence: that the place we give to our money does not contradict our values.

Principle of transparency: provide regular and public information on all activities and their consequences.

Principle of involvement: ethical principles have a transversal dimension in the organization, not only in its activity, but also in its attitude and commitment.

They also say that they accept and promote the cooperative principles of the International Co-operative Alliance:

Open voluntary membership: Cooperatives are voluntary entities open to all persons capable of providing their services.

Democratic control of its members: Cooperatives are entities democratically managed by their members and actively participate in their policies and decision-making.

Economic participation of the partners: The members contribute just enough in the capital of their cooperatives and manage it democratically.

Autonomy and independence: cooperatives are autonomous self-help organizations managed by their members.

Education, training and information: Cooperatives provide training and training to members, selected representatives, directors and employees so that they can contribute effectively to the development of cooperatives.

Cooperation between cooperatives: cooperatives should jointly strengthen the cooperative movement.

Interest in the community: Cooperatives work to achieve the sustainable development of their communities.

Ask the bank where you keep your money to follow those Principles and see what they say.

Intrigued?

Coop57 might not work everywhere, as the laws of your jurisdiction are likely different than in Spain. Co-ops and Credit Unions in other countries might do similar work, but often hold themselves out to be banks like any other bank, just with a different mission.

But the limits to growth that Coop57 puts on itself ensures that it stays true to its mission. If you want to learn more, check them out for yourself. If you want an organization like Coop57 where you live, what are you waiting for? Start one.

If you want to learn more in Spanish, you can watch this video where someone from Coop57 speaks in a cool accent - with tiny English Subtitles - COOP57 - YouTube

I’m guessing the people that run Coop57 might agree with you.

Very good article. I didn't know about coop57, thank you for enlightening me.

I only knew about SACCOSS which is kind of similar but different